Identity theft damages your credit score by placing fraudulent accounts, missed payments, and hard inquiries on your credit report that credit models treat as legitimate negative behavior. The Fair Credit Reporting Act gives you the right to dispute every one of those entries, but the process requires speed, documentation, and persistence. Credit bureaus like Equifax, Experian, and TransUnion do not automatically flag fraud. They report what lenders send them. That means the burden of correction falls on you, and the sooner you act, the less damage accumulates.

How identity theft affects credit score: the mechanics

Understanding exactly what happens to your credit file is the first step toward fixing it. Credit scoring models do not determine fault. They simply react to data. A fraudulent missed payment looks identical to a real one inside a FICO or VantageScore calculation. That is why the impact of identity theft on your credit can be severe and fast.

Here is what fraudulent activity typically introduces to your report:

- New unauthorized accounts. A thief opens a credit card or personal loan in your name. That new account lowers your average account age and adds a hard inquiry, both of which reduce your score.

- Delinquent or unpaid balances. When the thief stops paying, the account goes delinquent. Unpaid fraudulent accounts affect your creditworthiness and loan eligibility just as a real default would.

- Elevated credit utilization. Fraudulent balances push your utilization ratio higher. Utilization above 30% is a known score depressor across all major scoring models.

- Hard inquiries from fraud applications. Every credit application the thief submits generates a hard inquiry. Multiple inquiries in a short window signal risk to lenders and pull your score down further.

The core problem is that credit scoring models treat all credit information equally regardless of intent. Dispute focus must be on correcting the record, not establishing fault.

Each of these factors compounds the others. A thief who opens three accounts, maxes them out, and stops paying can trigger a score drop of 100 points or more within a few billing cycles. That kind of damage affects your ability to rent an apartment, qualify for a mortgage, or secure a car loan.

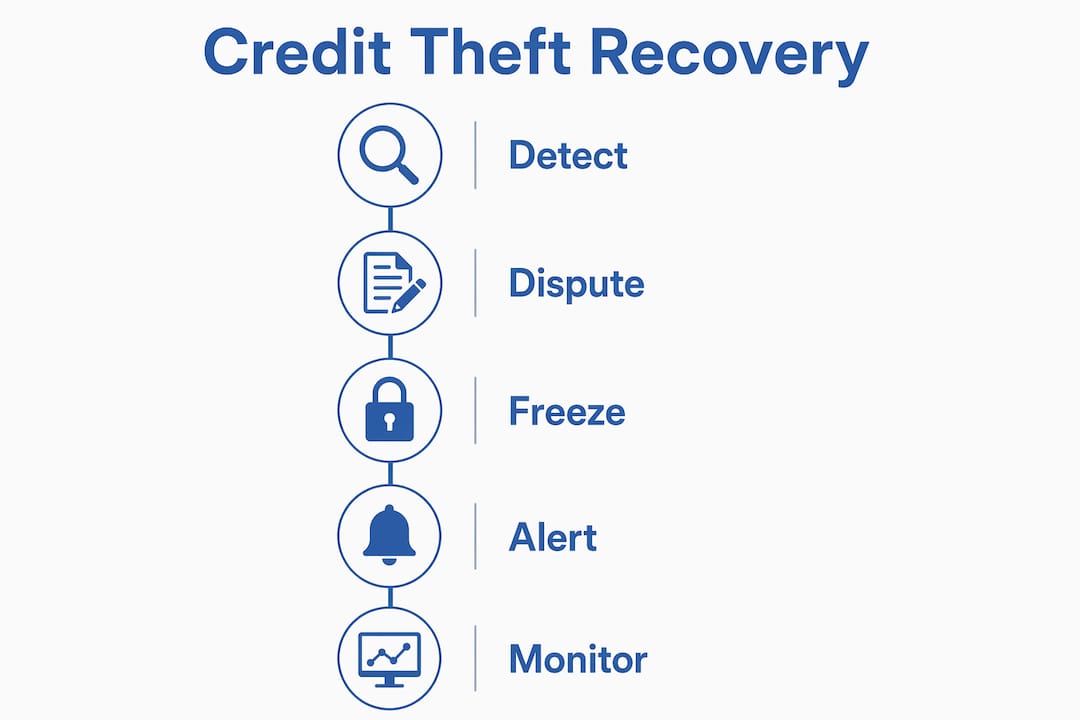

How do you detect identity theft errors on your credit reports?

You cannot fix what you cannot see. Catching fraud early is the single most effective way to limit how far your credit score falls.

Follow these steps to monitor your reports effectively:

- Pull all three reports at once. Visit AnnualCreditReport.com, where free weekly access to reports from Equifax, Experian, and TransUnion is permanently available. Checking all three matters because not every lender reports to every bureau.

- Look for accounts you did not open. Scan the accounts section for any creditor name you do not recognize. Even a small store card you never applied for is a red flag.

- Check the inquiries section. Hard inquiries from lenders you never contacted indicate someone applied for credit in your name. One unfamiliar inquiry is suspicious. Two or more is a clear warning sign.

- Review payment history line by line. A missed payment on an account you did not know existed confirms fraudulent activity is already affecting your score.

- Set up real-time alerts. Services like Experian’s free credit monitoring or paid platforms reviewed at Techstacktoday send alerts the moment a new account or inquiry appears. Do not wait for your monthly statement to find out.

Pro Tip: Set a recurring calendar reminder to pull your reports every four weeks. Rotating through the three bureaus monthly means you are effectively checking your file every ten days on average.

Knowing how to detect identity theft early gives you the best chance of containing the damage before it compounds. Most victims discover fraud months after it begins, which is why proactive monitoring matters more than reactive checking.

What steps fix fraudulent information on your credit report?

Disputing errors is not a one-step process. Consumers often must follow up to confirm corrections and re-dispute if fraudulent data reappears. Go in with realistic expectations and a system.

Here is how to approach it:

- Start at IdentityTheft.gov. This FTC-managed site creates a recovery plan tailored to your situation and generates an official identity theft report you will need for every dispute you file.

- File disputes with all three bureaus separately. Equifax, Experian, and TransUnion each maintain independent files. A correction at one does not automatically carry to the others. Submit your dispute to each one individually with supporting documentation.

- Build a case packet. The FTC advises including copies of your identity theft report, account statements, correspondence with lenders, and any police report. A thorough evidence packet reduces the number of rounds required and speeds correction.

- Track every communication. Log the date, method, and content of every dispute submission and every response. If a bureau re-reports the same fraudulent item after removing it, your records are your proof.

- Follow up in writing. Bureaus have 30 days to investigate disputes. If you do not receive a response or the item is not corrected, send a follow-up letter referencing your original submission date.

Pro Tip: Request a free updated credit report from each bureau immediately after a dispute resolves. Confirm the fraudulent item is gone before closing the case. Errors can reappear if the original lender re-reports the data.

Your identity theft recovery steps should run in parallel with protective measures. Disputing past damage while leaving your file open to new fraud is like bailing out a boat without plugging the hole.

Credit freezes vs. fraud alerts: which one actually protects you?

These two tools serve different purposes. Choosing the right one depends on how much protection you need right now.

| Feature | Credit Freeze | Fraud Alert |

|---|---|---|

| What it does | Blocks all lender access to your credit file | Flags your file so lenders must verify your identity |

| How strong is the protection | Prevents new accounts entirely | Reduces risk but does not block access |

| Cost | Free at all three bureaus | Free at all three bureaus |

| Duration | Indefinite until you lift it | 1 year (extended alert available for victims) |

| Where to apply | Separately at Equifax, Experian, and TransUnion | One bureau notifies the other two |

| Impact on existing accounts | None | None |

A credit freeze blocks lender access completely until you lift it. No one can open a new account in your name while a freeze is active, regardless of how much of your personal data has been exposed. That makes it the stronger long-term option.

A fraud alert is easier to manage. Placing one at any single bureau triggers automatic alerts at all three. Lenders who see the flag are required to take extra steps to verify your identity before approving credit. However, a determined thief with enough of your information can still get through.

Freezes prevent new accounts regardless of how much data a thief holds. Fraud alerts are a lighter layer. For most identity theft victims, the right move is to place a freeze immediately and add a fraud alert as a secondary signal. Neither option affects your existing credit cards, loans, or accounts in any way.

What proactive steps protect your credit going forward?

Recovery is only half the work. Protecting your credit from future theft requires building habits that make you a harder target.

- Enroll in credit monitoring. Services that watch all three bureaus and alert you in real time catch new fraud within hours instead of months. Techstacktoday reviews and ranks the best identity protection services based on hands-on testing, not paid placements.

- Use a password manager. Weak or reused passwords are one of the most common entry points for account takeovers. Tools like Bitwarden, 1Password, or Dashlane generate and store strong, unique credentials for every account.

- Run dark web scans. Many identity protection services include dark web monitoring that alerts you when your email, Social Security number, or financial data appears in breach databases.

- Use a VPN on public networks. Public Wi-Fi at airports, hotels, and coffee shops exposes your data to interception. A VPN encrypts your connection and prevents thieves from capturing login credentials or financial information in transit.

- Be selective with personal information. Limit what you share on social media and be skeptical of unsolicited requests for your Social Security number, date of birth, or account numbers. Phishing emails and fake websites remain the most common methods thieves use to harvest credentials.

- Check your reports regularly. Even with a freeze in place, reviewing your reports every month catches errors, outdated information, and any fraud that slipped through before the freeze was placed.

Key takeaways

Identity theft causes direct, measurable credit score damage because scoring models treat fraudulent activity exactly like legitimate negative behavior, making fast action and documented disputes the only path to recovery.

| Point | Details |

|---|---|

| Fraud hits scores fast | Fraudulent missed payments and new accounts lower your score within one billing cycle. |

| Disputes require all three bureaus | File separately with Equifax, Experian, and TransUnion; corrections do not transfer automatically. |

| Freezes outperform fraud alerts | A credit freeze fully blocks new account openings; a fraud alert only flags lenders to verify identity. |

| Evidence packets speed recovery | Include your FTC identity theft report, statements, and all correspondence in every dispute submission. |

| Monitoring prevents repeat damage | Real-time credit alerts catch new fraud before it compounds into larger score damage. |

The uncomfortable truth about credit recovery after identity theft

Here is what most articles skip: the dispute process is slow, and it often requires more than one round. Fraudulent items can reappear on your report after a bureau removes them if the original lender re-reports the data without updating their records. That is not a glitch. It is a structural gap in how the credit reporting system works.

The FTC is clear that illegal credit repair shortcuts like filing false identity theft reports to wipe legitimate negative items can result in criminal charges. Social media is currently full of influencers pushing exactly this tactic. Avoid it completely. It makes your situation worse, not better.

What actually works is methodical documentation combined with a credit freeze placed on day one. The victims who recover fastest are not the ones who found a shortcut. They are the ones who pulled all three reports immediately, filed at IdentityTheft.gov within 24 hours, and kept a paper trail of every dispute and response.

Credit repair companies cannot legally remove accurate negative information, and they charge significant fees for work you can do yourself for free. The FTC confirms that consumers can fix credit themselves through timely, documented disputes. Save your money and invest your time instead.

One more thing: do not wait for a dramatic sign. A single unfamiliar hard inquiry on your report is enough reason to freeze your file today. The cost is zero. The protection is real.

— TechStackTeam

Protect your credit with tools Techstacktoday has already tested

Techstacktoday has hands-on tested over 50 privacy and identity protection services so you do not have to sort through marketing claims on your own. If you are ready to take action, start with our ranked list of identity protection services covering real-time credit monitoring, dark web scanning, and fraud alerts. For securing your online activity and stopping data interception before it starts, our independently tested VPN reviews identify the fastest and most private options available right now. And if weak passwords are part of your exposure, our guide to the best password managers covers the tools that actually hold up under real-world testing.

FAQ

How fast does identity theft lower your credit score?

Fraudulent accounts and missed payments can lower your score within a single billing cycle, typically 30 to 60 days after the fraudulent activity begins. The more accounts a thief opens, the faster and steeper the drop.

Can you fully recover your credit score after identity theft?

Yes. Once you successfully dispute and remove all fraudulent items from your Equifax, Experian, and TransUnion reports, your score will recover to reflect your actual credit history. Full recovery can take several months depending on how long the fraud went undetected.

Does placing a credit freeze hurt your credit score?

No. A credit freeze has zero impact on your existing credit score, accounts, or loans. It only prevents new lenders from accessing your file to open new accounts.

What is the first thing to do when you suspect identity theft?

Pull your credit reports from all three bureaus at AnnualCreditReport.com, then file a report at IdentityTheft.gov to generate an official identity theft report and recovery plan. Place a credit freeze at Equifax, Experian, and TransUnion immediately after.

Are credit repair companies worth using after identity theft?

No. Credit repair companies cannot legally remove accurate negative information, and the FTC confirms consumers can dispute fraudulent items themselves for free. Paid services offer no legal advantage over a well-documented self-filed dispute.