Most people assume that if someone steals their identity and drains their bank account, their identity theft insurance will pay them back. That belief is wrong, and it costs victims real money. Understanding the role of identity protection reimbursement means knowing exactly what is and is not covered before a crisis hits. This article breaks down what reimbursement actually covers, how claims work, what policies look like side by side, and what steps to take if you need to file. No confusion. No surprises.

Table of Contents

- Key takeaways

- The role of identity protection reimbursement

- How reimbursement actually works

- Comparing identity protection policies

- Common misconceptions about reimbursement

- Practical steps for victims filing claims

- My honest take on identity protection reimbursement

- Protect yourself with the right coverage

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Reimbursement covers recovery costs | Identity theft insurance pays for legal fees, lost wages, and admin costs — not stolen funds. |

| Claims require documentation | You must save receipts, logs, and proof of theft to avoid partial or denied claims. |

| Policy limits vary widely | Standard coverage runs $25,000 to $50,000 per incident, with sub-limits on specific expenses. |

| Monitoring and insurance differ | Credit monitoring prevents theft; reimbursement insurance helps you recover after it happens. |

| Scams target victims post-theft | No legitimate service guarantees recovery of stolen funds or asks for upfront fees. |

The role of identity protection reimbursement

Let’s clear up the most common misunderstanding right away. Identity protection reimbursement, known in the insurance industry as identity theft insurance, is an indemnity product. That means it covers recovery expenses, not the stolen money itself. Your bank or credit card company handles fraudulent transaction reversals. Your identity theft insurance covers the work it takes to fix everything else.

Here is what typical reimbursement policies actually cover:

- Legal fees for attorneys helping dispute fraudulent accounts or charges

- Lost wages for time taken off work to handle the recovery process, often with sub-limits of $250 to $500 per day

- Notarization and certified mailing costs for sending affidavits and dispute letters

- Loan reapplication fees if fraudulent accounts caused a denial

- Credit monitoring subscriptions purchased during recovery

What it does not cover: the $4,000 someone wired out of your checking account. Insurance excludes the stolen funds themselves, along with pain and suffering damages and lost investments.

Here is a concrete example. Say your Social Security number was used to open three credit cards. You spend two days off work making calls, hire an attorney to send cease-and-desist letters, and pay $85 in certified mailing fees. Your identity theft policy reimburses those costs. The fraudulent credit card balances? Those get disputed directly with the card issuers and do not come out of your insurance.

Pro Tip: Before you buy any identity protection policy, read the sub-limits carefully. A policy with a $25,000 total limit but only $500 for attorney fees will leave you exposed when legal help matters most.

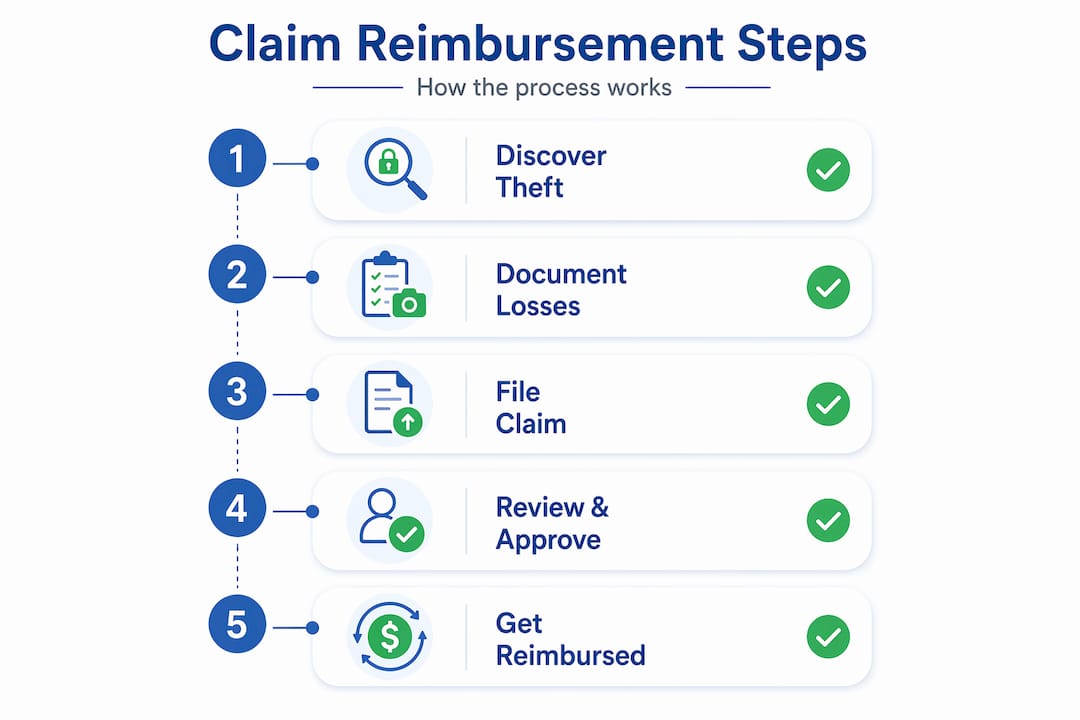

How reimbursement actually works

Understanding the mechanics prevents nasty surprises when you file. Reimbursement is retrospective by design. You pay the expense first, then submit documentation to the insurer, who verifies the claim and pays you back. There is no advance fund to draw from.

Here is how the claims process typically unfolds:

- Report the identity theft to the FTC at IdentityTheft.gov and file a police report. Both documents are standard requirements for any claim.

- Track every expense from day one. Keep receipts for mailing, legal consultations, and any services you paid for during recovery.

- Contact your insurer as soon as possible. Most policies have a reporting window, and missing it can void your claim.

- Submit a formal claim packet with your FTC report, police report, itemized expense list, and all receipts.

- Wait for verification. The insurer reviews your documentation and either approves, partially approves, or denies the claim.

Claims get denied or reduced when documentation is incomplete. Insufficient evidence of the theft or missing receipts are the top reasons insurers reject claims. It is not about bad faith. It is about meeting the policy’s evidentiary standard.

Common exclusions to watch for:

- Pain and suffering: Emotional distress is not included in coverage

- Lost investments: If fraud caused you to miss a market opportunity, that loss is not reimbursable

- Pre-existing theft: If the identity theft occurred before your policy started, you are not covered

- Business losses: Most personal policies exclude losses tied to self-employment or business accounts

Pro Tip: Create a dedicated folder, physical or digital, the moment you discover identity theft. Every receipt, every call log, every email goes in there. Organized documentation is the single biggest factor in a smooth claim.

Comparing identity protection policies

Not all policies are created equal. The difference between a basic add-on and a full-service plan can mean tens of thousands of dollars in coverage and dozens of hours of saved recovery work.

| Feature | Basic add-on | Mid-tier plan | Premium plan |

|---|---|---|---|

| Reimbursement limit | Up to $25,000 | $25,000 to $50,000 | $1,000,000+ |

| Lost wages sub-limit | $250/day | $500/day | $1,000+/day |

| Recovery specialist | No | Sometimes | Yes, dedicated |

| Credit monitoring | No | 1 bureau | 3 bureaus |

| Legal fee coverage | Limited | Moderate | Full |

Standard homeowners or renters policies typically bundle identity theft coverage at the $25,000 to $50,000 range per incident. That covers most recovery situations for individuals. However, if your case involves complex fraud or drawn-out legal disputes, you will want a higher-tier standalone plan.

Data breach settlements also offer a form of reimbursement worth knowing about. The Fidelity Data Breach settlement, for example, offers up to $5,000 for documented losses plus two years of credit monitoring and $1 million in identity theft insurance. These settlements are separate from personal policies and require their own claim submissions.

Additional identity protection policy benefits to look for:

- Access to dedicated recovery specialists who handle disputes on your behalf

- Three-bureau credit monitoring with real-time alerts

- Dark web scanning to detect exposed credentials before fraud occurs

- Social Security number monitoring across financial databases

Professional recovery specialists save victims hundreds of hours navigating creditor disputes, credit bureau corrections, and government agency paperwork. That alone makes premium plans worth the price difference for many people. You can compare plans with strong reimbursement benefits at Techstacktoday’s ranked identity protection services.

Common misconceptions about reimbursement

Misinformation here does not just cause confusion. It leaves you financially exposed and vulnerable to scams.

Myth #1: My insurance will pay back stolen money.

It will not. Financial institutions handle fraudulent transaction reversals. Your insurance covers the cost of proving the fraud and fixing your records.

Myth #2: A recovery service can guarantee I get my money back.

No legitimate organization can guarantee that. Any service claiming guaranteed results and asking for upfront payment is a predatory scam. These operations specifically target identity theft victims who are already distressed and desperate.

⚠️ If someone contacts you after a data breach and promises to recover your stolen funds for a fee paid upfront, do not engage. Legitimate recovery services never charge upfront fees. Report the contact to the FTC immediately.

Myth #3: Identity protection insurance replaces monitoring.

They serve completely different functions. Monitoring detects threats early. Reimbursement insurance helps you recover after a confirmed theft. You need both, not one or the other.

Myth #4: I can handle the recovery myself and avoid needing insurance.

You can try. But modern AI-enabled identity theft creates increasingly complex fraud chains that can take months to unravel. Professional recovery support has become far more valuable as the fraud itself has become more sophisticated.

Know your rights. The Fair Credit Reporting Act gives you the right to dispute inaccurate information. The FTC provides free recovery plans at IdentityTheft.gov. Understanding these protections makes you a stronger advocate for yourself.

Practical steps for victims filing claims

If you are currently dealing with identity theft, here is what to do right now.

- Report immediately. File with the FTC and your local police department. Get the report numbers. You will need them.

- Contact your insurer. Notify them within the policy’s required window. Ask exactly what documentation they need.

- Log every expense. Date, amount, purpose, receipt. Do this every single day from discovery forward.

- Use your recovery specialist. If your plan includes one, activate that benefit immediately. Let them handle creditor calls and bureau disputes. Careful documentation maximizes your reimbursement and a specialist knows exactly what to capture.

- Freeze your credit. Contact Equifax, Experian, and TransUnion. A credit freeze stops new accounts from being opened in your name while you recover.

- Monitor continuously. Set up alerts on your remaining accounts and check your credit reports weekly during the recovery period.

After submitting your claim, do not go quiet. Follow up with your insurer every five to seven business days. Ask for written status updates. If a claim is partially denied, request the specific reason in writing and provide additional documentation to appeal.

Pro Tip: When choosing a new identity protection policy, prioritize plans that include a dedicated recovery specialist over those that only offer a call center. Specialist access is where the real value is, especially if your case gets complicated.

For a deeper look at what happens right after your data is exposed, Techstacktoday’s guide on what to do after a breach walks you through the first 24 hours step by step.

My honest take on identity protection reimbursement

I have spent years reviewing identity protection services at Techstacktoday, and the single biggest mistake I see readers make is treating reimbursement insurance as a safety net for stolen funds. It is not. Once I understood it as a recovery expense tool, not a financial backstop, everything else clicked.

What actually concerns me is how many people have bare-bones identity theft add-ons through their homeowners insurance and have no idea what the sub-limits are. A $250-per-day wage cap sounds reasonable until you realize a complex fraud case can consume three to four weeks of your work hours.

The recovery specialist benefit is where I see the most underappreciated value. In testing multiple services, the ones with dedicated specialists resolved disputes significantly faster than DIY approaches. The paperwork burden alone is enough to discourage most victims from pushing back on creditors effectively.

My honest advice: do not just buy insurance and move on. Pair it with active monitoring, strong passwords via a reliable password manager, and a clear understanding of your policy’s limits. Reimbursement is one piece of the recovery puzzle, not the whole picture.

— TechStackTeam

Protect yourself with the right coverage

At Techstacktoday, we have tested and ranked over 50 identity protection services based on real-world performance, not paid placements. Our hands-on reviews cover reimbursement limits, monitoring quality, recovery specialist access, and overall value. If you are unsure whether your current coverage is adequate, our top-rated identity protection services page gives you a clear, unbiased comparison to work from. We also review VPN services and password managers to help you build a complete privacy strategy. No fluff, no paid rankings. Just what actually works.

FAQ

What does identity theft reimbursement actually cover?

Identity theft reimbursement covers recovery-related expenses such as legal fees, lost wages, notarization costs, and mailing fees. It does not cover the stolen funds themselves, which are handled separately by your bank or credit card issuer.

How much does a standard identity protection policy reimburse?

Standard coverage through homeowners or renters insurance typically runs $25,000 to $50,000 per incident. Premium standalone plans can offer $1 million or more, with higher sub-limits for legal fees and lost wages.

Can identity theft insurance guarantee I get stolen money back?

No. Identity theft insurance is an indemnity product covering recovery costs, not stolen funds. Any service guaranteeing stolen fund recovery in exchange for an upfront fee is a scam.

What documentation do I need to file a reimbursement claim?

You need a filed FTC identity theft report, a police report, itemized receipts for all recovery expenses, and written proof of the identity theft incident. Incomplete documentation is the most common reason claims are denied or reduced.

Is credit monitoring the same as identity theft insurance?

No. Credit monitoring alerts you to suspicious activity so you can catch theft early. Identity theft insurance reimburses the costs you incur after theft has already occurred. Both serve different purposes and work best when used together.