Something feels off. Maybe a charge you don’t recognize showed up on your bank statement, or you got a letter about a loan you never applied for. Figuring out how to know if my identity was stolen is not always obvious, and that uncertainty is exactly what makes identity theft so damaging. The good news: there are clear, concrete warning signs across your financial accounts, tax records, mail, and medical history. This guide walks you through each one, plus the exact steps to take if something looks wrong.

Table of Contents

- Key takeaways

- How to know if my identity was stolen: financial red flags

- Tax-related identity theft signs

- Warning signs in your mail and medical records

- Tools and steps to check for stolen identity

- What to do if you suspect identity theft

- My take on what most people get wrong

- Protect yourself with the right tools

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Watch your credit closely | A sudden 50-point drop in your credit score with no personal reason is a major red flag. |

| Check your credit reports now | Pull free reports from AnnualCreditReport.com to spot unfamiliar accounts or hard inquiries. |

| Tax filings can reveal fraud | An IRS rejection notice for a duplicate Social Security number means someone filed a return using your identity. |

| Mail disappearance matters | Missing bank statements or credit card bills can signal a fraudster changed your address to hide activity. |

| Act fast with a freeze and report | Place a credit freeze, file an FTC report, and contact your bank immediately after suspecting theft. |

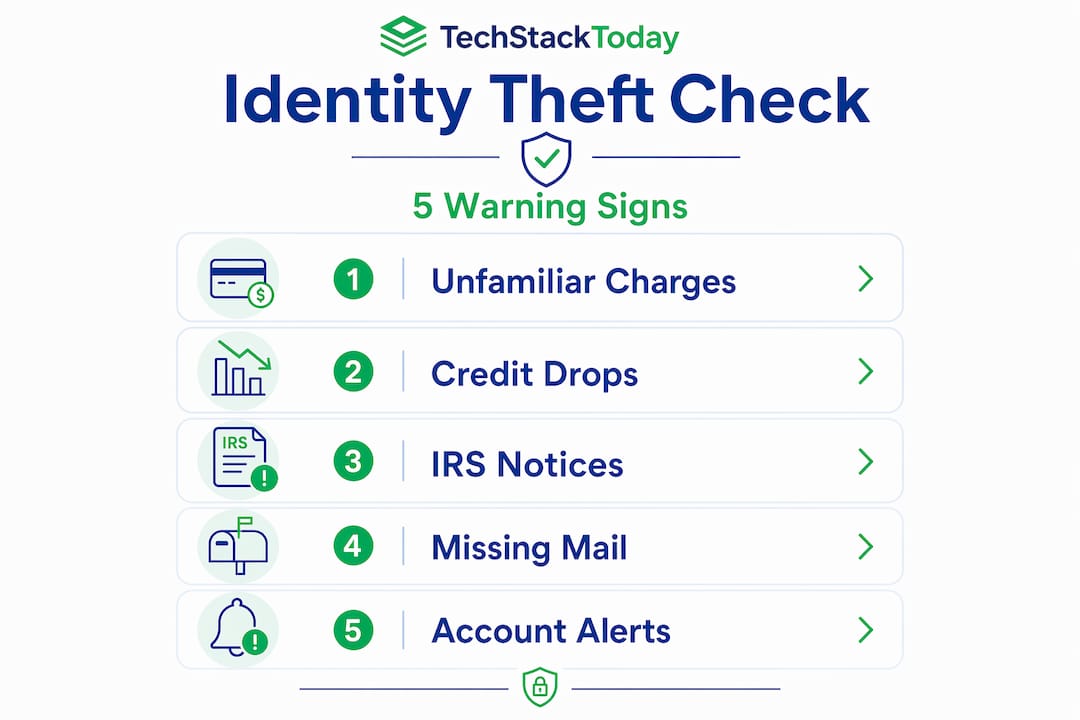

How to know if my identity was stolen: financial red flags

Your bank and credit accounts are usually the first place identity theft shows up. The signs are not always dramatic. Sometimes it is a small, unfamiliar charge you almost scroll past.

Here is what to look for:

- Unrecognized transactions. Any purchase, transfer, or withdrawal you did not make is a problem. Thieves often test stolen card numbers with tiny charges before making larger ones.

- Unfamiliar hard credit inquiries. A hard inquiry means someone applied for credit in your name. If you see lenders you have never contacted on your credit report, that is a serious identity theft warning sign.

- Sudden credit score drop. A 50-point or greater drop with no related action on your part, like opening a new account or missing a payment, is a critical indicator.

- New accounts you did not open. Loans, credit cards, or lines of credit appearing on your report that you never applied for signal new account fraud.

- Maxed-out credit limits. If a card you rarely use suddenly shows a high balance, someone else may be spending on it.

There are two distinct types of fraud to understand here. Account takeover fraud means a thief gains access to an existing account. New account fraud means they use your personal information to open entirely new accounts in your name. Both show up on credit reports differently, which is why reviewing your full report matters, not just your score.

You are legally entitled to a free annual credit report from each of the three major bureaus through AnnualCreditReport.com. Pull all three, because not every creditor reports to every bureau.

Pro Tip: Space your three free credit reports throughout the year, one every four months, so you get a fresh look at your credit activity regularly without paying for monitoring.

Tax-related identity theft signs

Tax identity theft is one of the sneakiest forms of fraud because you often do not find out until you try to file your own return.

Watch for these specific signals:

- IRS rejection notice. If the IRS rejects your e-filed return because a return with your Social Security number was already submitted, someone beat you to it. The IRS flagged approximately 1.1 million potentially fraudulent returns in fiscal year 2022 alone.

- Unexpected tax transcripts. If you request your IRS tax transcript and see a filed return for a year you have not yet filed, that is fraud.

- Notices about income you did not earn. An IRS letter referencing wages from an employer you have never worked for means someone used your Social Security number for employment.

- Refund delays with no explanation. The IRS may hold your refund if it detects suspicious duplicate activity tied to your number.

⚠️ Important: If you suspect tax identity theft, request an IRS Identity Protection PIN (IP PIN) immediately. This six-digit number is required on your future returns and prevents anyone else from filing under your Social Security number. You can request one at IRS.gov.

The IRS has specific recovery steps for tax identity theft victims, including Form 14039, the Identity Theft Affidavit. Filing this form puts the IRS on notice and starts the investigation process. Do not wait for the IRS to contact you. If something looks wrong, act first.

Warning signs in your mail and medical records

Physical mail is one of the most overlooked indicators of identity theft. Mail disappearance is a reliable early warning sign that many victims ignore until the damage is done.

Look for these signals:

- Missing statements. If your monthly bank or credit card statements stop arriving, a thief may have submitted a change-of-address request to redirect your mail. This delays your awareness of fraudulent activity by weeks or months.

- Unexpected new cards or account letters. Receiving a card or welcome letter for an account you never opened is a direct sign of new account fraud.

- Explanation of Benefits (EOB) for treatments you did not receive. Your health insurer sends an EOB after every claim. Check each EOB for medical services you never had. This is how medical identity theft surfaces.

- Collection notices for unknown debts. A debt collector calling about a bill you do not recognize often means a fraudulent account has gone delinquent in your name.

Medical identity theft is particularly damaging because fraudulent records can alter your actual medical history. If you suspect it, request a full copy of your medical records from every provider and your insurer. Review each entry. Errors in your medical file can affect your care, your insurance rates, and your coverage eligibility.

Pro Tip: Sign up for USPS Informed Delivery, a free service that emails you a daily preview of incoming mail. If mail is previewed but never arrives, you have a concrete record to report.

Tools and steps to check for stolen identity

Knowing the warning signs is one thing. Having a system to actively check for stolen identity is what actually catches theft early.

Here is a comparison of the main tools available to you:

| Tool | What it catches | Cost |

|---|---|---|

| AnnualCreditReport.com | New accounts, hard inquiries, address changes | Free |

| HaveIBeenPwned.com | Email and password exposure in data breaches | Free |

| Credit bureau fraud alerts | Flags lenders to verify identity before extending credit | Free |

| Credit freeze | Blocks new credit applications entirely | Free |

| Identity protection services | Dark web monitoring, alerts, fraud resolution | Paid |

Start with the free options. Check HaveIBeenPwned.com to see if your email address appears in known data breach databases. If it does, change the passwords for every account using that email immediately.

Set up account-change alerts on every financial account you own. Most banks and brokerages allow you to receive instant notifications for address changes, password resets, and phone number updates. Enabling these alerts is one of the most effective ways to catch account takeover in real time.

Enable multi-factor authentication (MFA) everywhere it is offered. MFA means that even if a thief has your password, they cannot access your account without a second verification step. Use an authenticator app rather than SMS when possible, since SIM-swapping attacks can intercept text messages.

A credit freeze is your strongest tool for blocking new account fraud. It prevents any lender from pulling your credit to approve a new application. However, credit freezes do not block synthetic identity fraud or takeovers of existing accounts. Treat it as one layer, not the whole solution.

Pro Tip: Freeze your credit at all three bureaus, Equifax, Experian, and TransUnion, plus ChexSystems if you want to block fraudulent bank account openings. Each requires a separate request.

For deeper protection, consider reviewing your exposure on data broker sites. These sites compile and sell your personal information, and removing your data from them reduces the number of places a thief can find your details in the first place.

What to do if you suspect identity theft

Do not wait for certainty. If something looks wrong, start the process now. Here is your identity theft checklist:

- File a report with the FTC. Go to IdentityTheft.gov. The FTC generates a personalized recovery plan and an official Identity Theft Report, which you will need for the next steps.

- File a local police report. Some creditors and institutions require a police report number to process fraud disputes. Bring your FTC report with you.

- Place a fraud alert or credit freeze. A standard fraud alert lasts one year. An extended fraud alert lasts 7 years and requires a police or FTC report. A freeze is stronger and blocks new credit entirely.

- Contact your bank and credit card issuers. Report unauthorized charges. Ask to speak directly with the fraud department, not general customer service. Fraud departments have authority that general support staff do not.

- Dispute fraudulent accounts with the credit bureaus. Submit disputes in writing with your FTC report attached. The bureau must investigate within 30 days.

- Contact the IRS if tax fraud is suspected. Submit Form 14039 and request an IP PIN at IRS.gov.

- Document everything. Keep records of every call, every letter, and every dispute. Note the date, the representative’s name, and what was said.

Pro Tip: Create a dedicated folder, physical or digital, for all identity theft correspondence. Disputes can take months to resolve, and having organized records speeds up every step.

My take on what most people get wrong

I’ve reviewed dozens of identity theft cases and privacy services at Techstacktoday, and the pattern I keep seeing is the same. People assume a credit freeze is enough and stop there. It is not.

What I’ve learned is that synthetic identity fraud and retirement account takeovers are the two fastest-growing threats that a freeze does nothing to stop. In one documented case, a fraudster drained $751,430 from a 401(k) in a single phone call by impersonating the account holder. The victim had a credit freeze in place. It did not matter.

My experience tells me that the most underrated protection is alert setup. Most people have never turned on account-change notifications. That one step, taking about five minutes per account, would catch the majority of takeover attempts before they escalate.

The other thing I’ve noticed: people wait too long to report. They want to be sure before they make the call. But the FTC report costs you nothing and starts the clock on your legal protections. File it the moment something looks wrong. You can always update the details later.

— TechStackTeam

Protect yourself with the right tools

If you’ve made it through this guide, you already know more than most people about how to detect identity theft. Now it is time to put the right tools in place before something goes wrong.

At Techstacktoday, we test and rank privacy services based on real performance, not paid placements. Our reviews of identity protection services cover monitoring depth, alert speed, and fraud resolution quality so you know exactly what you are getting. We also rank the best password managers to help you lock down your accounts with strong, unique credentials, and we review VPN services that reduce your exposure on public networks. Every recommendation is based on hands-on testing. No sponsored rankings.

FAQ

How can I check if my identity was stolen for free?

Pull your free credit reports from AnnualCreditReport.com and check HaveIBeenPwned.com to see if your email appears in known data breaches. Both are free and take under 10 minutes.

What are the first signs of identity theft?

The most common early identity theft warning signs include unrecognized charges on your accounts, unfamiliar hard inquiries on your credit report, and missing mail like bank statements or credit card bills.

What should I do first if I suspect my identity was stolen?

File a report at IdentityTheft.gov immediately. The FTC generates an official Identity Theft Report and a personalized recovery plan, both of which you will need to dispute accounts and place an extended fraud alert.

Does a credit freeze fully protect me from identity theft?

No. A credit freeze blocks new credit applications but does not prevent account takeover fraud, synthetic identity fraud, or tax identity theft. It is one important layer within a broader protection strategy.

How do I know if someone filed taxes using my Social Security number?

If the IRS rejects your e-filed return because a return with your Social Security number was already submitted, that is a direct sign of tax identity theft. Request an IP PIN from IRS.gov to prevent future fraudulent filings.